Full Coverage vs. Liability Only: Do You Actually Need Both?

You are buying car insurance online. You see a checkbox for “Full Coverage” that costs $150/month, and one for “Liability Only” that costs $60/month.

The temptation to save that $90 is huge. But before you click “Liability Only,” you need to know exactly what happens if you crash.

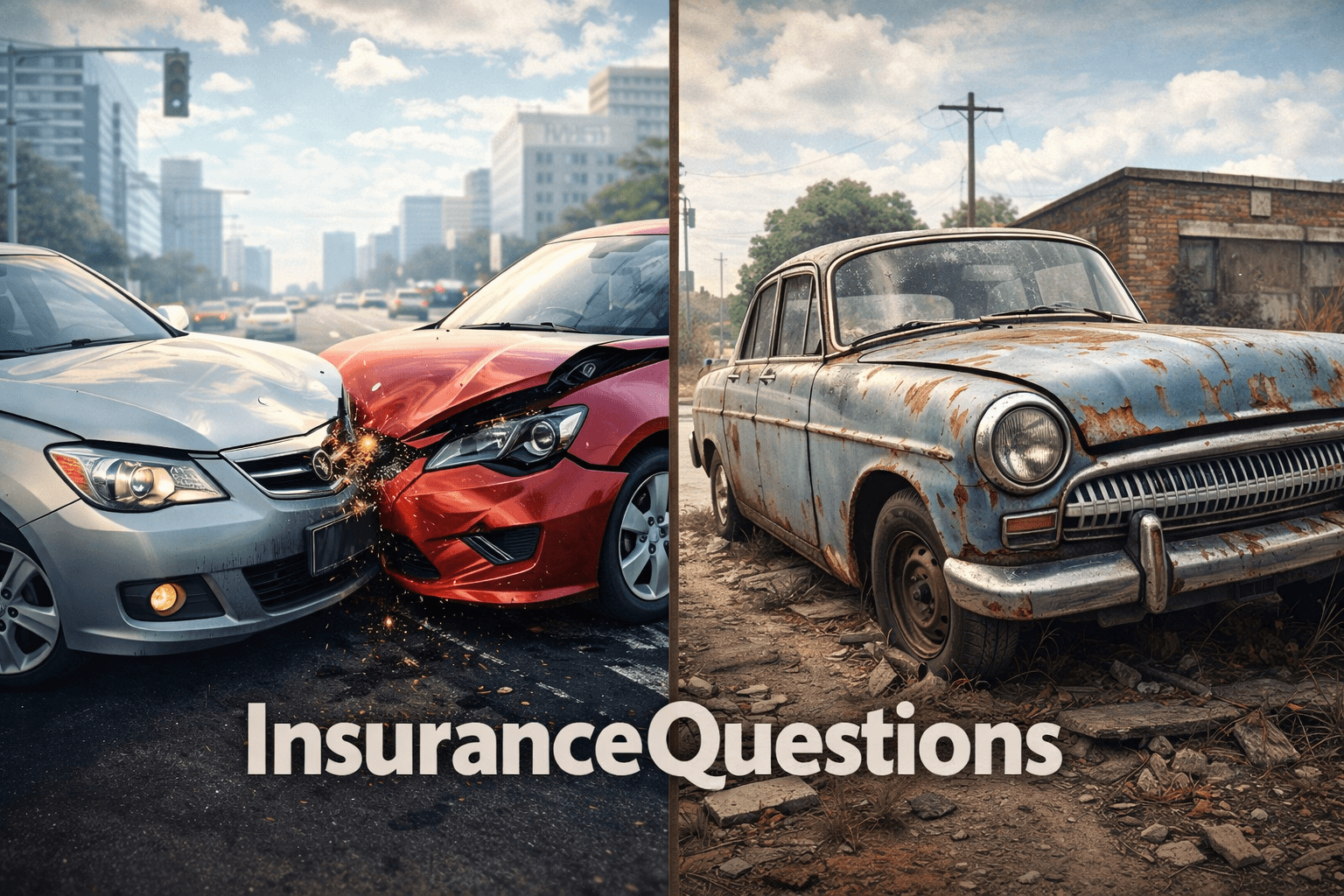

Liability Only: Protecting “The Other Guy”

If you have Liability Only and you smash into a Lexus, your insurance company will pay to fix the Lexus. They will pay for the other driver’s whiplash.

But your car? You are on your own.

If your front bumper is hanging off, or if your car is totaled, the insurance company will send you exactly $0.

- Who is this for? This is for people driving “beaters.” If you are driving a 2005 Honda Civic worth $1,500, it makes no sense to pay $1,000 a year to insure it.

Full Coverage: Protecting You

“Full Coverage” isn’t actually a technical term. It usually means you added two things: Collision and Comprehensive.

- Collision: Fixes your car if you hit another car (or a tree, or a mailbox).

- Comprehensive: Fixes your car if “bad luck” happens. Think theft, fire, hail damage, or hitting a deer.

The “10% Rule” of Thumb

How do you decide? Do a quick math problem.

Take the current market value of your car (check Kelley Blue Book). If the cost of “Full Coverage” for one year is more than 10% of your car’s value, it might be time to drop it.

For example:

- Car Value: $4,000

- Cost of Full Coverage extra per year: $600

- Wait, $600 is 15% of $4,000. That’s a bad deal. You might be better off saving that money for a new car fund instead.

Insurance is about math, not feelings. Don’t insure a rust bucket like it’s a Ferrari.